Assimilating loan agreements to bonds: is the Ethiopian Tax Authority prepared to levy duties on loan agreements?

Tibebe Zewdu

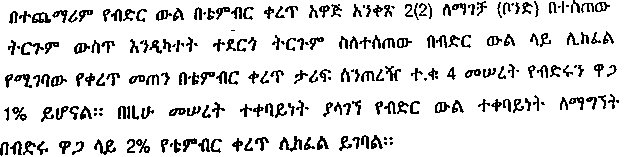

The Ministry of Revenues has recently issued an explanatory note on the Directive for Keeping of Books of Accounts for Tax Purposes, Directive No. – 176/2014. In this explanatory note, the Authority has extended the definition given to the term “bond” under the Stamp Duty Proclamation to include “loan agreements”. Below is an excerpt of the relevant section from the explanatory note:

This is worrying, to say the least, on many fronts because extension of the definition of a “bond” to “loans” in this manner is being used to levy a 1% stamp duty on all loan agreements executed in Ethiopia.

It is known that one of the instruments that are subject to stamp duty under the Ethiopian Stamp Duty Proclamation No. 110/1998 is a bond (“ማገቻ” in Amharic). The definition given to the term under the law is as follows:

“Bond” includes any instrument, whereby a person obliges himself to pay money to another, on condition that the obligation shall be void, if a specific act is performed or is not performed, as the case may be; or any instrument attested to by a witness and not payable to order or bearer, whereby a person obliges himself to pay money to another.

Two alternative definitions are given here to the term. One indicates an instrument under which a person promises to make payment based on the occurrence or non-occurrence of a particular event, while the other implies the same promise to make payment but with two important elements: attestation of the document by a witness, and the instrument not being negotiable.

While the first limb of the definition depicts the classic nature of bonds, one can see the prospect by which the second definition might be construed in a way that encompasses ordinary loan agreements provided these agreements are attested by witnesses.

In one sense, bonds and loan agreements are related in the sense that both attest an obligation to pay to a creditor, but there are important differences between loans and bonds.

The major difference between a bond and a loan agreement is the nature of the instruments that create them. A bond implies and sometimes presupposes the existence of another obligation when created to enforce such obligation. In this sense, bonds are forms of security instruments where they will be rendered unusable when the principal obligation ceases to exist.

A loan agreement on the other hand creates the obligation of the borrower to repay the loan itself. At the back of a bond, there is another obligation whose performance is guaranteed by the issuance of the instrument of a bond, while a loan is not connected (at least officially) with another obligation. Most loan agreements are not backed up by bonds as instruments.

At the back of the issuance of bail bonds is the promise to produce a person to a court, at the back of issuance of performance bonds is the guarantee to perform certain contractual obligations, such as construction of a road or a building.

Sometimes, bonds elevate a loan agreement into a security instrument. The bonds elevate the loan given from a mere personal obligation to a security instrument that not only guarantees payment but turns the bonds into negotiable instruments to be transferred to others. In the case of government bonds, for example, the government puts forth its creditworthiness to elevate ordinary one-to-one loan agreements into government bonds which represent a promise to pay the principal and interest to any bondholder.

At the back of loans, on the other hand, there is nothing but an obligation to return the money taken with or without interest. If a creditor demands a security for the repayment of the loan, a creditor demands another commitment from the borrower in the form of security agreements, which are considered as security deeds, attracting a stamp duty of 1% just like bonds (noting that transactions that create security rights governed by the Movable Property Security Right Proclamation are exempted from payment of this stamp duty).

Another feature that distinguishes bonds from loans is the fact that bonds can only be issued by larger corporations or government entities.

The question is if ordinary loan agreements not backed by bonds or security deeds should attract stamp duties. The idea of written loan agreements attested by two witnesses constituting “bonds” was long buried in the definition of “bonds” of the Stamp Duty Proclamation, now resurrected by the Explanatory Note of the MoRs. Even if we decide to set these differences aside, one should be able to anticipate the controversial actions of demanding payment of a 1% stamp duty on every loan agreement executed in Ethiopia.

We invite our followers to reflect and let us know their takes on this issue.

Transition to Performance-Based Investment Incentives under Regulation No. 586/2026

1. BACKGROUND Pursuant to the...

From Reform to Refinement: Ethiopia to Update the Directive on Foreign Participation in Restricted Export, Import, Wholesale and Retail Trade

The Ethiopian Investment Board...

A Landmark Development for Ethiopia’s Real Estate Sector

Sisay Habte and Michael...

Ethiopia’s Personal Data Protection Proclamation Enters in to Force

Bezawit Yirga and Benyam...

Fee Rates Payable for Services Provided by the Ethiopian Immigration and Nationality Service, under Council of Ministers Regulation No. 550/2024

Benyam Tafesse and Bezawit...